Research

August 07, 2026

Total U.S. jobs

U.S. job market disappointed in July, as labor participation continues to drop

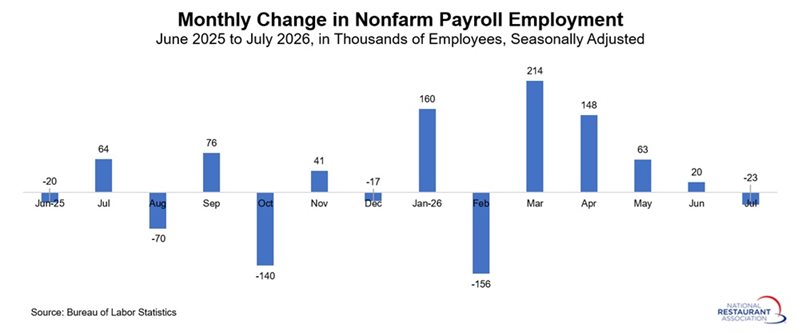

Nonfarm payroll employment declined by 23,000 in July, a disappointing result that fell well short of expectations, with consensus forecasts calling for an increase of roughly 80,000 jobs. Moreover, job growth in May and June was revised down significantly, with updated estimates reducing previously reported payroll gains by a combined 103,000 jobs.

Taken together, these figures suggest that the labor market has been softer than expected during the summer months following more solid employment gains in the spring. Although seasonal adjustment challenges and a declining labor force participation rate may be contributing to some of the recent weakness, the data still point to a cooling labor market that has the potential to weigh on consumer confidence and dampen the broader economic outlook.

Sustained growth in employment and wages remains essential to supporting household spending, which continues to be the primary driver of economic activity. Any meaningful deterioration in labor market conditions could restrain consumer expenditures and, in turn, slow overall economic growth.

Restaurant operators are closely monitoring these developments as they navigate softer-than-desired consumer demand. Continued labor market stability would help support spending patterns and restaurant traffic in the months ahead. If energy prices continue to moderate and consumer confidence steadies, the U.S. economy could still achieve modest growth in the second half of the year, accompanied by firmer labor market conditions.

At the same time, downside risks remain elevated amid ongoing geopolitical uncertainty and persistent inflationary pressures. These competing forces continue to complicate the Federal Reserve's policy calculus, as policymakers balance concerns about inflation against signs of a moderating labor market. While interest rates are still expected to move higher later this year, recent labor market weakness could provide justification for policymakers to remain on hold in the near term as they assess incoming economic data.

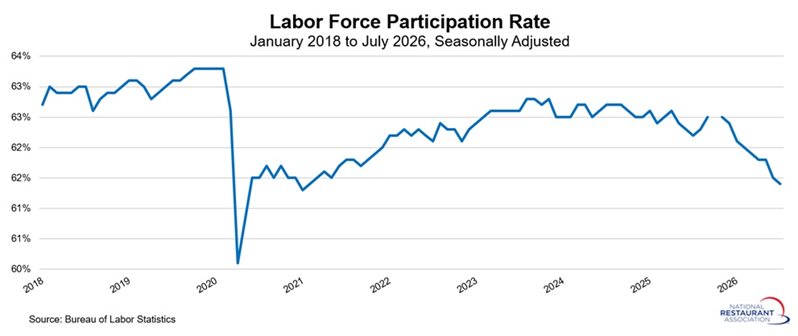

As noted above, labor force participation continues to move in the wrong direction. The civilian labor force declined from 171.50 million in December to 169.18 million in July, a reduction of 2.32 million workers over the past seven months. As a result, the labor force participation rate fell to 61.4% in July, its lowest level since February 2021. This trend suggests that a significant number of potential workers have moved to the sidelines, creating an ongoing challenge for employers. Even as broader labor market conditions show signs of cooling, many businesses, including restaurant operators, are likely to continue facing difficulties recruiting and retaining workers.

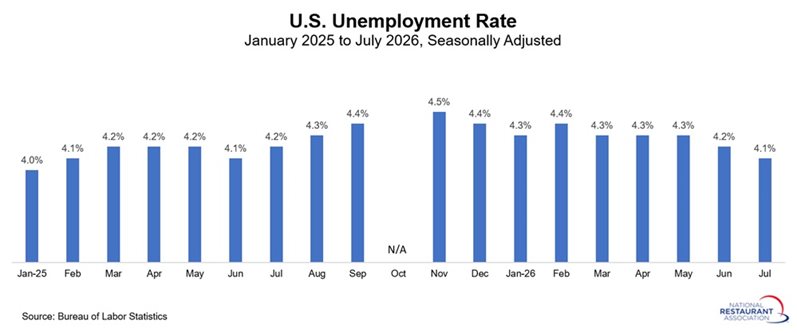

At the same time, the unemployment rate edged down from 4.2% in June to 4.1% in July, marking its lowest level in 13 months. On the surface, this suggests that the labor market remains relatively healthy by historical standards, even as net hiring remains weak. The number of unemployed individuals also declined, falling from 7.09 million in June to 6.92 million in July, the lowest level since January 2025.

Taken together, however, the decline in unemployment alongside a shrinking labor force suggests that at least some of the improvement in the jobless rate reflects fewer people participating in the labor market rather than a meaningful acceleration in hiring. As such, the lower unemployment rate may overstate the underlying strength of labor market conditions. Nonetheless, worker availability remains a key concern for employers across industries, particularly in labor-intensive sectors such as restaurants that depend on a steady pipeline of workers to support operations, growth, and customer demand.

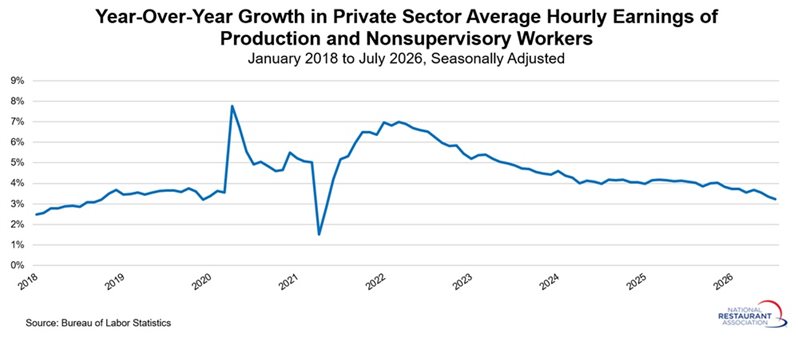

On the wage front, average hourly earnings for private-sector production and nonsupervisory workers edged up 0.1% in July to $32.40, rising 3.2% over the past 12 months. Monthly wage growth was the slowest since December, while year-over-year wage gains were the weakest since May 2021. Even with this moderation, wage growth remains relatively solid by historical standards, suggesting that workers continue to see income gains that can help support consumer spending.

Job growth in June was mixed but mostly weaker. The increase in employment was led by growth in private education and health services, construction, professional business services, and information. In contrast, there were notable decreases in local government, leisure and hospitality (including restaurants), retail trade, and financial activities. Below is a detailed breakdown of July’s employment changes by sector, ranked from highest to lowest:

Taken together, these figures suggest that the labor market has been softer than expected during the summer months following more solid employment gains in the spring. Although seasonal adjustment challenges and a declining labor force participation rate may be contributing to some of the recent weakness, the data still point to a cooling labor market that has the potential to weigh on consumer confidence and dampen the broader economic outlook.

Sustained growth in employment and wages remains essential to supporting household spending, which continues to be the primary driver of economic activity. Any meaningful deterioration in labor market conditions could restrain consumer expenditures and, in turn, slow overall economic growth.

Restaurant operators are closely monitoring these developments as they navigate softer-than-desired consumer demand. Continued labor market stability would help support spending patterns and restaurant traffic in the months ahead. If energy prices continue to moderate and consumer confidence steadies, the U.S. economy could still achieve modest growth in the second half of the year, accompanied by firmer labor market conditions.

At the same time, downside risks remain elevated amid ongoing geopolitical uncertainty and persistent inflationary pressures. These competing forces continue to complicate the Federal Reserve's policy calculus, as policymakers balance concerns about inflation against signs of a moderating labor market. While interest rates are still expected to move higher later this year, recent labor market weakness could provide justification for policymakers to remain on hold in the near term as they assess incoming economic data.

As noted above, labor force participation continues to move in the wrong direction. The civilian labor force declined from 171.50 million in December to 169.18 million in July, a reduction of 2.32 million workers over the past seven months. As a result, the labor force participation rate fell to 61.4% in July, its lowest level since February 2021. This trend suggests that a significant number of potential workers have moved to the sidelines, creating an ongoing challenge for employers. Even as broader labor market conditions show signs of cooling, many businesses, including restaurant operators, are likely to continue facing difficulties recruiting and retaining workers.

At the same time, the unemployment rate edged down from 4.2% in June to 4.1% in July, marking its lowest level in 13 months. On the surface, this suggests that the labor market remains relatively healthy by historical standards, even as net hiring remains weak. The number of unemployed individuals also declined, falling from 7.09 million in June to 6.92 million in July, the lowest level since January 2025.

Taken together, however, the decline in unemployment alongside a shrinking labor force suggests that at least some of the improvement in the jobless rate reflects fewer people participating in the labor market rather than a meaningful acceleration in hiring. As such, the lower unemployment rate may overstate the underlying strength of labor market conditions. Nonetheless, worker availability remains a key concern for employers across industries, particularly in labor-intensive sectors such as restaurants that depend on a steady pipeline of workers to support operations, growth, and customer demand.

On the wage front, average hourly earnings for private-sector production and nonsupervisory workers edged up 0.1% in July to $32.40, rising 3.2% over the past 12 months. Monthly wage growth was the slowest since December, while year-over-year wage gains were the weakest since May 2021. Even with this moderation, wage growth remains relatively solid by historical standards, suggesting that workers continue to see income gains that can help support consumer spending.

Job growth in June was mixed but mostly weaker. The increase in employment was led by growth in private education and health services, construction, professional business services, and information. In contrast, there were notable decreases in local government, leisure and hospitality (including restaurants), retail trade, and financial activities. Below is a detailed breakdown of July’s employment changes by sector, ranked from highest to lowest:

- Private education and health services: +25,000

- Construction: +22,000

- Professional and business services: +18,000

- Information: +11,000

- Other services: +9,000

- State government: +7,000

- Manufacturing: +5,000

- Mining and logging: -2,000

- Federal government: -3,000

- Trade, transportation, and utilities: -4,000 (retail trade: -19,400)

- Financial activities: -14,000

- Leisure and hospitality: -40,000 (eating and drinking places: -26,100)

- Local government: -57,000