Research

July 02, 2026

Total U.S. jobs

U.S. labor market growth softened in June, as labor participation drops sharply

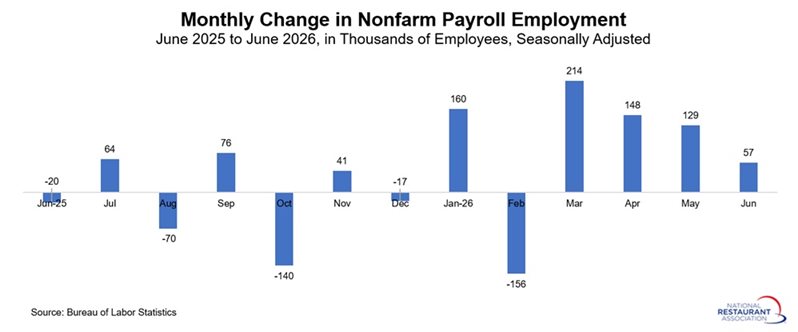

Nonfarm payroll employment increased by 57,000 in June, well below the consensus expectation of 118,000. In addition, April and May payroll estimates were revised downward by a combined 74,000 jobs. While the labor market entered the summer on a softer-than-expected note, employment has still increased in five of the first six months of the year, with payrolls up a net 552,000 year to date. That suggests the labor market remains resilient, even as hiring growth moderates.

Sustained gains in employment and wages remain critical to supporting consumer spending, and any meaningful deterioration in labor market conditions could weigh on broader economic activity. Restaurant operators are closely monitoring these trends as they contend with softer-than-desired consumer demand. Continued labor market strength would help support spending and restaurant traffic in the months ahead.

If energy costs continue to ease and consumer confidence stabilizes, the U.S. economy could see modest growth in the second half of the year, accompanied by firmer labor market conditions. However, downside risks remain elevated amid ongoing geopolitical uncertainty and persistent inflationary pressures. These crosscurrents complicate the Federal Reserve’s policy outlook, potentially reducing the likelihood of interest rate cuts this year and increasing the risk that policymakers maintain a restrictive stance for longer.

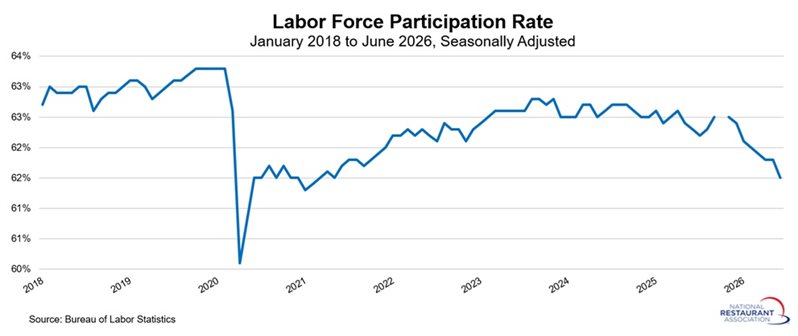

A notable development in the June employment report was the continued decline in labor force participation. The civilian labor force fell from 171.50 million in December 2025 to 169.36 million in June, a reduction of 2.14 million workers over the past six months. As a result, the labor force participation rate dipped to 61.5% in June, its lowest level since May 2021. This trend suggests that a significant number of potential workers have moved to the sidelines, creating an ongoing challenge for employers. Even as broader labor market conditions show signs of cooling, many businesses—including restaurant operators—are likely to continue facing difficulties recruiting and retaining workers.

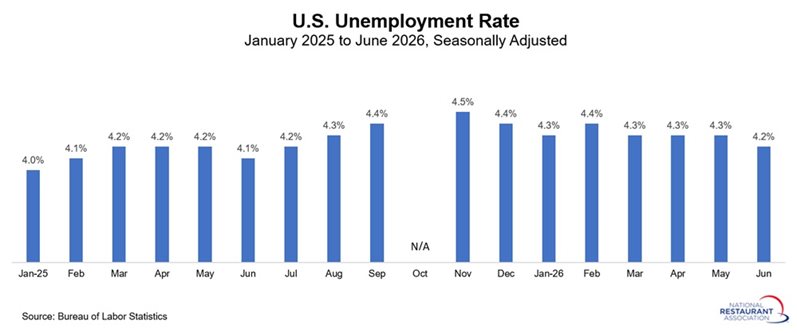

At the same time, the unemployment rate edged down from 4.3% in May to 4.2% in June, marking its lowest level in 11 months. Even with that improvement, the unemployment rate has averaged 4.3% during the first half of 2025, indicating a labor market that remains relatively healthy by historical standards. The number of unemployed individuals also declined, falling from 7.31 million in May to 7.09 million in June.

Taken together, the drop in unemployment alongside a shrinking labor force suggests that part of the improvement in the jobless rate reflects fewer people participating in the labor market rather than a broad-based acceleration in hiring. Nonetheless, labor availability remains a key concern for employers across industries, particularly in sectors such as restaurants that continue to depend on a stable pipeline of workers to support operations and growth.

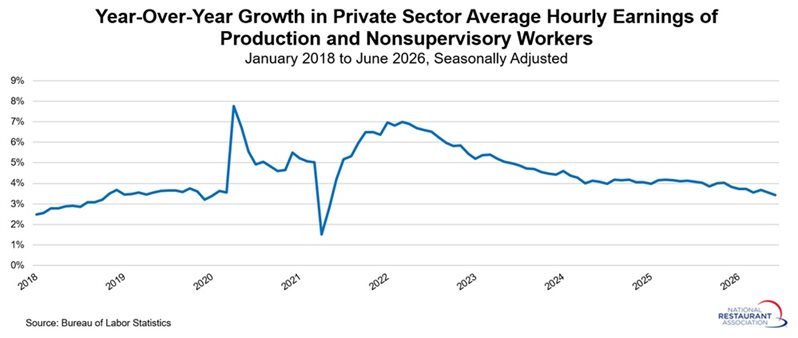

On the wage front, average hourly earnings for private‑sector production and nonsupervisory workers rose 0.2% to $32.38 in June, up 3.4% from a year earlier. That was the slowest pace of wage growth since May 2021. Still, this suggests a still-solid rate of wage growth in the U.S. economy, even as labor cost pressures have eased markedly from their peaks of 7.8% in April 2020, in the immediate aftermath of the pandemic, and 7.0% in January and March 2022.

Job growth in June was mixed. The increase in employment was led by growth in private education and health services, professional business services, and construction. In contrast, there were notable decreases in leisure and hospitality (including restaurants), information, and retail trade. Below is a detailed breakdown of June’s employment changes by sector, ranked from highest to lowest:

Sustained gains in employment and wages remain critical to supporting consumer spending, and any meaningful deterioration in labor market conditions could weigh on broader economic activity. Restaurant operators are closely monitoring these trends as they contend with softer-than-desired consumer demand. Continued labor market strength would help support spending and restaurant traffic in the months ahead.

If energy costs continue to ease and consumer confidence stabilizes, the U.S. economy could see modest growth in the second half of the year, accompanied by firmer labor market conditions. However, downside risks remain elevated amid ongoing geopolitical uncertainty and persistent inflationary pressures. These crosscurrents complicate the Federal Reserve’s policy outlook, potentially reducing the likelihood of interest rate cuts this year and increasing the risk that policymakers maintain a restrictive stance for longer.

A notable development in the June employment report was the continued decline in labor force participation. The civilian labor force fell from 171.50 million in December 2025 to 169.36 million in June, a reduction of 2.14 million workers over the past six months. As a result, the labor force participation rate dipped to 61.5% in June, its lowest level since May 2021. This trend suggests that a significant number of potential workers have moved to the sidelines, creating an ongoing challenge for employers. Even as broader labor market conditions show signs of cooling, many businesses—including restaurant operators—are likely to continue facing difficulties recruiting and retaining workers.

At the same time, the unemployment rate edged down from 4.3% in May to 4.2% in June, marking its lowest level in 11 months. Even with that improvement, the unemployment rate has averaged 4.3% during the first half of 2025, indicating a labor market that remains relatively healthy by historical standards. The number of unemployed individuals also declined, falling from 7.31 million in May to 7.09 million in June.

Taken together, the drop in unemployment alongside a shrinking labor force suggests that part of the improvement in the jobless rate reflects fewer people participating in the labor market rather than a broad-based acceleration in hiring. Nonetheless, labor availability remains a key concern for employers across industries, particularly in sectors such as restaurants that continue to depend on a stable pipeline of workers to support operations and growth.

On the wage front, average hourly earnings for private‑sector production and nonsupervisory workers rose 0.2% to $32.38 in June, up 3.4% from a year earlier. That was the slowest pace of wage growth since May 2021. Still, this suggests a still-solid rate of wage growth in the U.S. economy, even as labor cost pressures have eased markedly from their peaks of 7.8% in April 2020, in the immediate aftermath of the pandemic, and 7.0% in January and March 2022.

Job growth in June was mixed. The increase in employment was led by growth in private education and health services, professional business services, and construction. In contrast, there were notable decreases in leisure and hospitality (including restaurants), information, and retail trade. Below is a detailed breakdown of June’s employment changes by sector, ranked from highest to lowest:

- Private education and health services: +69,000

- Professional and business services: +36,000

- Construction: +11,000

- Other services: +8,000

- State government: +4,000

- Manufacturing: +3,000

- Federal government: +2,000

- Local government: +2,000

- Financial activities: unchanged

- Mining and logging: -4,000

- Trade, transportation, and utilities: -4,000 (retail trade: -7,500)

- Information: -9,000

- Leisure and hospitality: -61,000 (eating and drinking places: -32,900)