Research

July 30, 2026

PCE Deflator

Lower energy costs reduced PCE inflation in June, while spending has shown resilience year to date

The Personal Consumption Expenditures (PCE) deflator, the Federal Reserve’s preferred measure of inflation, declined 0.1% in June after posting solid gains throughout the spring. The decrease was driven largely by a 9.1% drop in gasoline and other energy prices, reflecting a pause in hostilities related to the conflict with Iran and following significant increases over the previous three months. Even with June’s decline, gasoline and other energy prices remained 26.4% higher than a year ago.

In contrast, prices for food and beverages purchased for off-premises consumption rose 0.3% in June and were up 2.4% over the past 12 months. Meanwhile, the data suggest that menu prices increased at a robust pace in the second quarter, advancing at a 3.2% annualized rate.

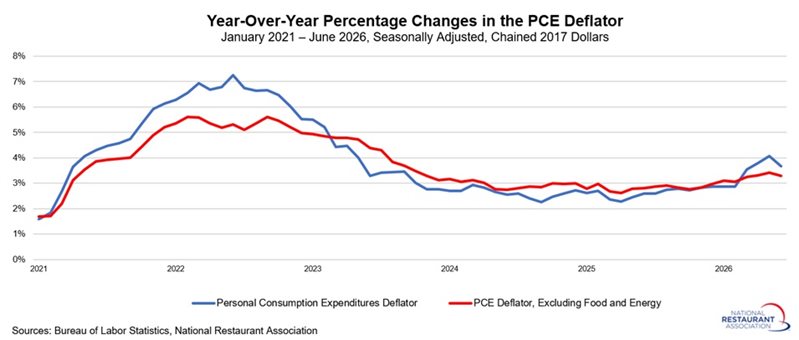

On a year-over-year basis, the headline PCE deflator eased to 3.7% in June, down from 4.1% in May, which was the fastest pace of inflation since April 2023. Core PCE inflation, which excludes food and energy, inched up 0.1% in June, down from 0.3% in May. Over the past 12 months, core inflation slipped from 3.4% year-over-year in May, its highest reading since October 2023, to 3.3% in June.

Overall, these data suggest that reduced energy costs helped to ease pricing pressures in June. With that said, hostilities have resumed in the war in Iran, with energy costs rising again in July. In addition, inflation has largely trended upward over the past year.

This poses a challenge for the Federal Reserve, especially as price growth continues to drift further from its long-run 2% target. Policymakers have struck a more hawkish tone in recent communications, reflecting renewed concern about inflation. While interest rates are likely to remain unchanged in the near term, there is growing speculation that rates may need to rise later this year if inflation continues to run above levels deemed acceptable by the Federal Open Market Committee.

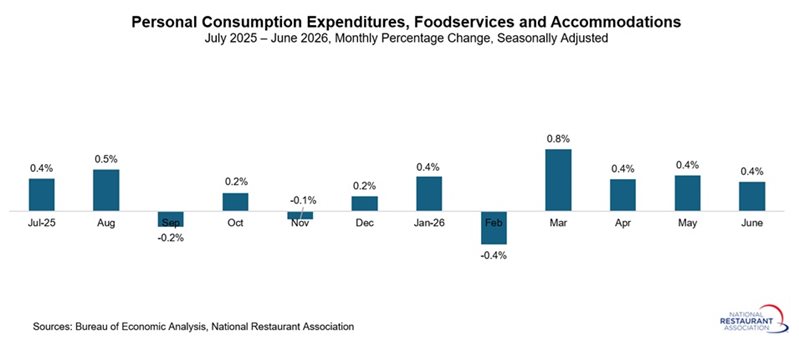

Consumer spending continued to expand in June, with personal consumption expenditures rising 0.3%. While that marked the slowest monthly increase since January, it still reflects a healthy pace of spending following robust gains throughout the spring. In nominal terms, consumer demand has remained resilient over the past five months despite elevated gasoline prices, weaker consumer confidence, and broader economic uncertainty. Higher tax refunds likely provided additional support, particularly earlier in the spring. Spending on foodservices and accommodations increased 0.4% in June, matching the gains seen in each of the prior two months.

Over the past 12 months, total personal spending rose a solid 6.3%. Spending on foodservices and accommodations increased a more modest 3.0% during that period, suggesting that consumers continue to dine out and travel, but with somewhat greater caution amid ongoing economic headwinds and softer recent readings.

Importantly, a meaningful portion of this spending growth reflects higher prices rather than stronger purchasing activity. After adjusting for inflation, real personal consumption increased 2.5% from a year earlier. Real spending on foodservices and accommodations edged up 0.1% in June and was 0.6% higher than a year ago, underscoring continued, albeit more moderate, growth in discretionary consumer spending.

Personal incomes rose 0.2% in June, slowing from 0.7% growth in May. Overall, personal income grew by 3.9% over the past 12 months. Wages, which have been a large contributor to the economy’s resilience, increased 0.2% in May, with 4.3% growth year-over-year.

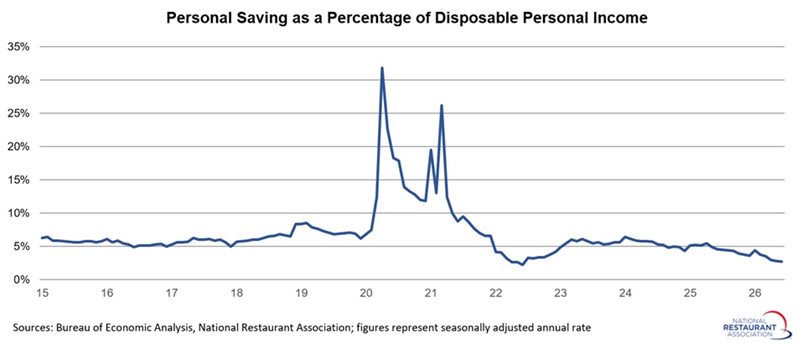

With spending outpacing income growth, the personal savings rate dropped from 2.8% in May to 2.7% in June, the lowest in four years. Overall, the savings rates in the post‑pandemic period remain well below historical norms. Prior to the pandemic, the savings rate averaged 6.5% from 2017 to 2019, compared with an average of just 3.7% over the past 12 months. This suggests that consumers are dipping into their savings to finance their spending.

In contrast, prices for food and beverages purchased for off-premises consumption rose 0.3% in June and were up 2.4% over the past 12 months. Meanwhile, the data suggest that menu prices increased at a robust pace in the second quarter, advancing at a 3.2% annualized rate.

On a year-over-year basis, the headline PCE deflator eased to 3.7% in June, down from 4.1% in May, which was the fastest pace of inflation since April 2023. Core PCE inflation, which excludes food and energy, inched up 0.1% in June, down from 0.3% in May. Over the past 12 months, core inflation slipped from 3.4% year-over-year in May, its highest reading since October 2023, to 3.3% in June.

Overall, these data suggest that reduced energy costs helped to ease pricing pressures in June. With that said, hostilities have resumed in the war in Iran, with energy costs rising again in July. In addition, inflation has largely trended upward over the past year.

This poses a challenge for the Federal Reserve, especially as price growth continues to drift further from its long-run 2% target. Policymakers have struck a more hawkish tone in recent communications, reflecting renewed concern about inflation. While interest rates are likely to remain unchanged in the near term, there is growing speculation that rates may need to rise later this year if inflation continues to run above levels deemed acceptable by the Federal Open Market Committee.

Consumer spending continued to expand in June, with personal consumption expenditures rising 0.3%. While that marked the slowest monthly increase since January, it still reflects a healthy pace of spending following robust gains throughout the spring. In nominal terms, consumer demand has remained resilient over the past five months despite elevated gasoline prices, weaker consumer confidence, and broader economic uncertainty. Higher tax refunds likely provided additional support, particularly earlier in the spring. Spending on foodservices and accommodations increased 0.4% in June, matching the gains seen in each of the prior two months.

Over the past 12 months, total personal spending rose a solid 6.3%. Spending on foodservices and accommodations increased a more modest 3.0% during that period, suggesting that consumers continue to dine out and travel, but with somewhat greater caution amid ongoing economic headwinds and softer recent readings.

Importantly, a meaningful portion of this spending growth reflects higher prices rather than stronger purchasing activity. After adjusting for inflation, real personal consumption increased 2.5% from a year earlier. Real spending on foodservices and accommodations edged up 0.1% in June and was 0.6% higher than a year ago, underscoring continued, albeit more moderate, growth in discretionary consumer spending.

With spending outpacing income growth, the personal savings rate dropped from 2.8% in May to 2.7% in June, the lowest in four years. Overall, the savings rates in the post‑pandemic period remain well below historical norms. Prior to the pandemic, the savings rate averaged 6.5% from 2017 to 2019, compared with an average of just 3.7% over the past 12 months. This suggests that consumers are dipping into their savings to finance their spending.