Research

July 29, 2026

Monetary Policy

Federal Reserve leaves rates unchanged but with a possible rate hike later in 2026

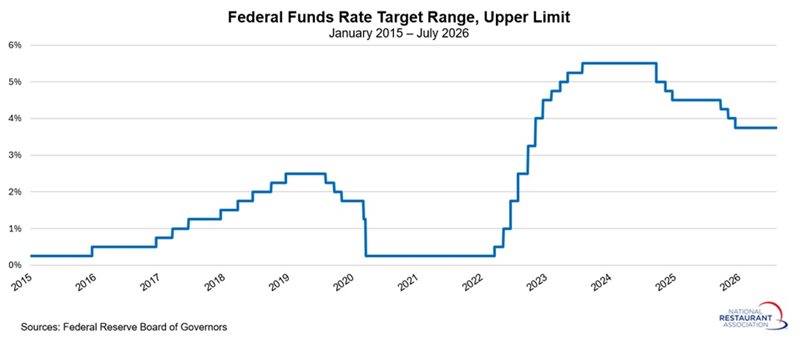

At its July 28–29 meeting, the Federal Open Market Committee (FOMC) left short-term interest rates unchanged, marking the fifth consecutive meeting without a policy move following three straight 25-basis-point cuts at the end of 2025. As a result, the federal funds rate remains in a target range of 3.50% to 3.75%.

The FOMC again emphasized that inflation remains a concern, with price growth continuing to exceed the Federal Reserve’s 2% long-term target. The Committee noted that elevated inflation is due “in part reflecting supply shocks that have driven price increases in certain sectors, including energy.” Members also reiterated their commitment to restoring price stability.

Notably, three regional Federal Reserve Bank presidents—Beth M. Hammack (Cleveland), Neel Kashkari (Minneapolis), and Lorie K. Logan (Dallas)—dissented from the decision, preferring to raise the federal funds rate by 25 basis points. Their votes underscored growing concerns that inflationary pressures could prove more persistent than previously anticipated.

On a more positive note, the FOMC highlighted continued economic resilience, citing solid growth despite “elevated uncertainty that owes, in part, to the conflict in the Middle East.” The Committee also pointed to healthy gains in employment, productivity, and capital investment.

Looking ahead, inflation remains the key risk factor. Recent data suggest that price pressures are moving in the wrong direction, at least for now. If inflation remains more elevated than the Committee would like, the prospect of rate hikes later this year will increase. Financial markets are already pricing in the possibility of one or two rate increases.

The most likely path in the near term is a continued pause, with incoming economic data shaping policy decisions at the FOMC’s three remaining meetings this year, including its next gathering on September 15–16. The probability of at least one rate hike later this year, though, appears more likely than not, but that outlook could change as additional economic data become available.

For the restaurant industry, elevated interest rates continue to weigh on borrowing costs, often slowing expansion plans, renovations, and other capital investments. If a higher-rate environment materializes later this year, financing burdens could increase further, potentially dampening consumer spending and constraining demand in sectors that are particularly sensitive to discretionary income, including foodservice and hospitality.

The FOMC again emphasized that inflation remains a concern, with price growth continuing to exceed the Federal Reserve’s 2% long-term target. The Committee noted that elevated inflation is due “in part reflecting supply shocks that have driven price increases in certain sectors, including energy.” Members also reiterated their commitment to restoring price stability.

Notably, three regional Federal Reserve Bank presidents—Beth M. Hammack (Cleveland), Neel Kashkari (Minneapolis), and Lorie K. Logan (Dallas)—dissented from the decision, preferring to raise the federal funds rate by 25 basis points. Their votes underscored growing concerns that inflationary pressures could prove more persistent than previously anticipated.

On a more positive note, the FOMC highlighted continued economic resilience, citing solid growth despite “elevated uncertainty that owes, in part, to the conflict in the Middle East.” The Committee also pointed to healthy gains in employment, productivity, and capital investment.

Looking ahead, inflation remains the key risk factor. Recent data suggest that price pressures are moving in the wrong direction, at least for now. If inflation remains more elevated than the Committee would like, the prospect of rate hikes later this year will increase. Financial markets are already pricing in the possibility of one or two rate increases.

The most likely path in the near term is a continued pause, with incoming economic data shaping policy decisions at the FOMC’s three remaining meetings this year, including its next gathering on September 15–16. The probability of at least one rate hike later this year, though, appears more likely than not, but that outlook could change as additional economic data become available.

For the restaurant industry, elevated interest rates continue to weigh on borrowing costs, often slowing expansion plans, renovations, and other capital investments. If a higher-rate environment materializes later this year, financing burdens could increase further, potentially dampening consumer spending and constraining demand in sectors that are particularly sensitive to discretionary income, including foodservice and hospitality.