Research

July 30, 2026

GDP

U.S. economy grew 1.5% in Q2 as consumer and business spending rebounded

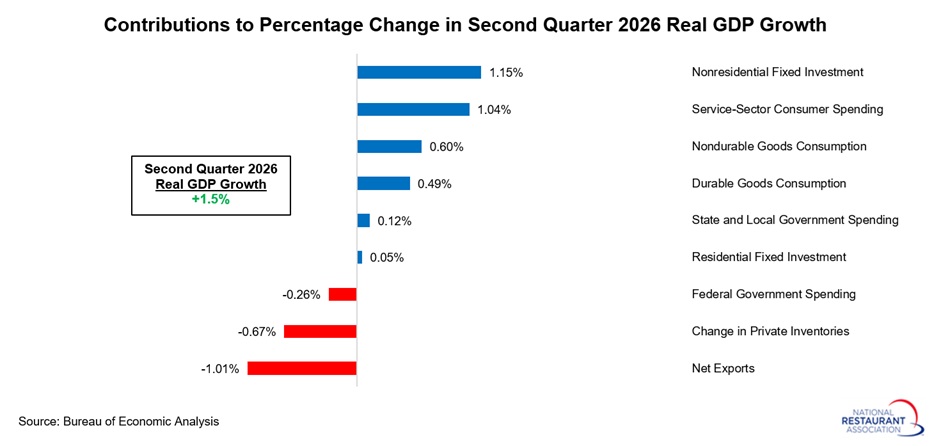

The U.S. economy expanded at a 1.5% annualized rate in the second quarter of 2026, slowing from 2.1% growth in the first quarter and coming in slightly below consensus expectations of 1.8%.

Beneath the headline figure, however, economic momentum was stronger than the GDP data alone would suggest. Consumer spending and fixed investment, key indicators of underlying domestic demand, increased at a robust 4.0% annual rate in the second quarter, more than double the 1.8% pace recorded in the first quarter. The acceleration points to a rebound in both household and business spending following two quarters of more subdued growth.

At the same time, overall GDP growth was restrained by several temporary drags, including a deterioration in net exports, slower inventory accumulation, and a decline in federal government spending.

Looking ahead, the National Restaurant Association expects the economy to remain resilient. Real GDP is forecast to grow 2.1% in 2026, matching the pace of 2025, before accelerating to 2.5% growth in 2027. Nevertheless, economic uncertainty and affordability pressures are likely to persist, particularly as geopolitical tensions, including ongoing conflict involving Iran, continue to pose risks to the outlook.

Looking beneath the headline figures, consumer spending strengthened considerably in the second quarter, rising at a 3.2% annual rate after softer gains in the prior two quarters. Goods spending increased a robust 5.2%, the strongest pace since the fourth quarter of 2024, while spending on services advanced by a more modest 2.2%. Overall, personal consumption expenditures contributed 2.12 percentage points to real GDP growth in Q2, a sharp improvement from just 0.37 percentage points in the first quarter and a clear sign that consumers became more willing to spend.

Business investment also remained a bright spot, although overall investment activity was mixed. Fixed investment increased at a healthy 7.0% annual rate in Q2, building on a 6.5% gain in the first quarter. As in the previous quarter, growth was driven by strong increases in equipment investment (+15.2%) and intellectual property products investment (+8.8%), reflecting continued spending on artificial intelligence and other productivity-enhancing technologies.

By contrast, investment in structures fell 5.0%, marking its tenth consecutive quarterly decline. One encouraging development was residential investment, which rose 1.5% and posted its first increase since the fourth quarter of 2024. Meanwhile, businesses scaled back inventory accumulation after modest stockpiling in recent quarters. As a result, gross private domestic investment contributed 0.53 percentage points to GDP growth in Q2, down from 1.35 percentage points in Q1.

Trade remained a headwind for economic growth. Net exports reduced real GDP growth by 1.01 percentage points in the second quarter, marking the third consecutive quarter in which trade weighed on the economy. Imports increased 11.5% at an annual rate, outpacing the 4.5% gain in exports and widening the trade drag on growth.

Government spending also exerted modest downward pressure on GDP. Federal government expenditures declined for the second time in the past three quarters, subtracting 0.27 percentage points from growth, with spending down 2.7% over the past year. In contrast, state and local government spending rose 1.1% at an annual rate, adding 0.12 percentage points to overall GDP growth, although that represented a slower pace than the 1.6% increase recorded in the first quarter.

Beneath the headline figure, however, economic momentum was stronger than the GDP data alone would suggest. Consumer spending and fixed investment, key indicators of underlying domestic demand, increased at a robust 4.0% annual rate in the second quarter, more than double the 1.8% pace recorded in the first quarter. The acceleration points to a rebound in both household and business spending following two quarters of more subdued growth.

At the same time, overall GDP growth was restrained by several temporary drags, including a deterioration in net exports, slower inventory accumulation, and a decline in federal government spending.

Looking ahead, the National Restaurant Association expects the economy to remain resilient. Real GDP is forecast to grow 2.1% in 2026, matching the pace of 2025, before accelerating to 2.5% growth in 2027. Nevertheless, economic uncertainty and affordability pressures are likely to persist, particularly as geopolitical tensions, including ongoing conflict involving Iran, continue to pose risks to the outlook.

Looking beneath the headline figures, consumer spending strengthened considerably in the second quarter, rising at a 3.2% annual rate after softer gains in the prior two quarters. Goods spending increased a robust 5.2%, the strongest pace since the fourth quarter of 2024, while spending on services advanced by a more modest 2.2%. Overall, personal consumption expenditures contributed 2.12 percentage points to real GDP growth in Q2, a sharp improvement from just 0.37 percentage points in the first quarter and a clear sign that consumers became more willing to spend.

Business investment also remained a bright spot, although overall investment activity was mixed. Fixed investment increased at a healthy 7.0% annual rate in Q2, building on a 6.5% gain in the first quarter. As in the previous quarter, growth was driven by strong increases in equipment investment (+15.2%) and intellectual property products investment (+8.8%), reflecting continued spending on artificial intelligence and other productivity-enhancing technologies.

By contrast, investment in structures fell 5.0%, marking its tenth consecutive quarterly decline. One encouraging development was residential investment, which rose 1.5% and posted its first increase since the fourth quarter of 2024. Meanwhile, businesses scaled back inventory accumulation after modest stockpiling in recent quarters. As a result, gross private domestic investment contributed 0.53 percentage points to GDP growth in Q2, down from 1.35 percentage points in Q1.

Trade remained a headwind for economic growth. Net exports reduced real GDP growth by 1.01 percentage points in the second quarter, marking the third consecutive quarter in which trade weighed on the economy. Imports increased 11.5% at an annual rate, outpacing the 4.5% gain in exports and widening the trade drag on growth.

Government spending also exerted modest downward pressure on GDP. Federal government expenditures declined for the second time in the past three quarters, subtracting 0.27 percentage points from growth, with spending down 2.7% over the past year. In contrast, state and local government spending rose 1.1% at an annual rate, adding 0.12 percentage points to overall GDP growth, although that represented a slower pace than the 1.6% increase recorded in the first quarter.

.jpg?lang=en-US "contributions-to-real-GDP-growth-(1).jpg")