Research

May 21, 2026

Economic outlook

U.S. economy poised to remain resilient in 2026 despite downside risks

The U.S. economy continues to send mixed signals—showing unexpectedly solid, albeit uneven, growth for now even as the labor market slows noticeably. When employment is strong and wages are rising, consumer spending typically remains resilient, including discretionary categories such as dining out. However, the evolving labor market underscores a key tension: while still relatively healthy, it represents a growing source of downside risk for restaurants and the broader economy.

At the same time, consumer confidence has fallen sharply, reaching a record low amid persistently elevated gasoline prices driven by the war in Iran. Even prior to the conflict, there were clear signs of consumer strain, with many households struggling to make ends meet, placing greater emphasis on affordability and becoming more deliberate in their spending decisions. Restaurant operators are increasingly concerned that higher gasoline prices will weigh on traffic and sales while further squeezing already tight profit margins. These pressures could be exacerbated if inflation remains elevated.

To be sure, there are also positive factors helping to mitigate these risks. Equity and housing values remain at or near all-time highs, and wages continue to rise at healthy, albeit moderating, rates. The “K-shaped” nature of consumer spending remains evident, supporting overall resilience, particularly among higher-income households. Meanwhile, larger tax refunds have provided some temporary relief, helping to offset higher costs associated with gasoline and other essential goods.

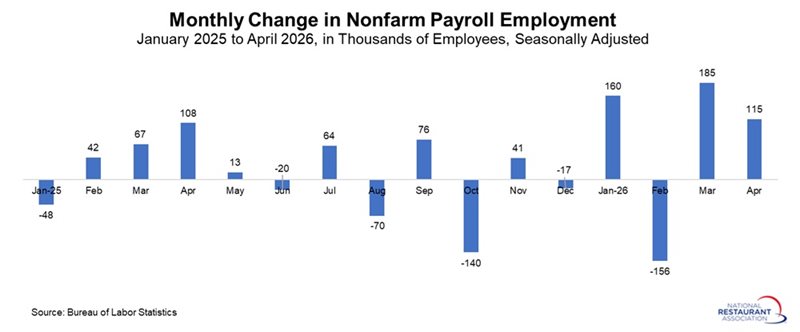

The labor market itself has been somewhat choppy. While hiring slowed in the second half of 2025, nonfarm payrolls increased by a solid 115,000 in April, with gains recorded in three of the first four months of 2026. We forecast that the U.S. economy will add approximately 750,000 net new jobs this year—a slower pace than in recent years but still indicative of underlying economic durability. At the same time, the unemployment rate remains historically low.

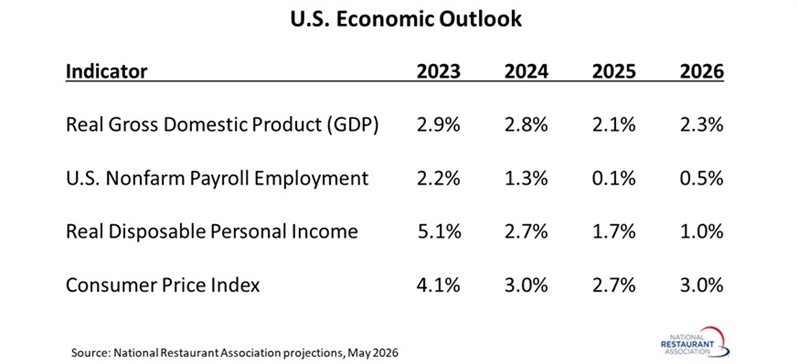

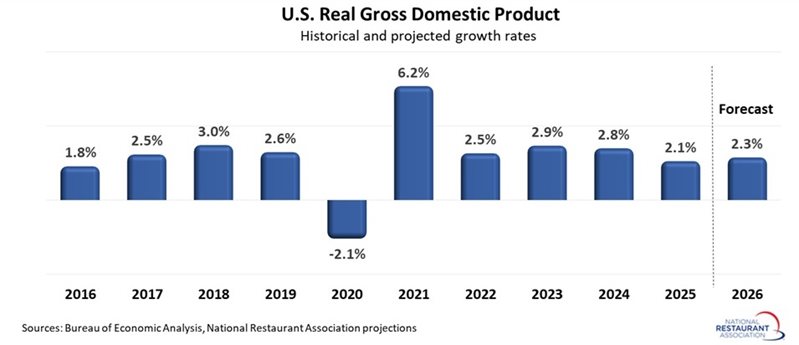

Looking ahead, the National Restaurant Association forecasts real GDP growth of 2.3% in 2026, slightly above the 2.1% pace expected for 2025. This outlook reflects continued resilience despite geopolitical risks and heightened caution among consumers and businesses. Growth has been supported in part by strong investment in artificial intelligence and data infrastructure, even as spending in other areas—particularly goods—has slowed or stalled.

Inflation, however, remains a complicating factor. Prices are expected to trend somewhat higher in the near term, placing the Federal Reserve in a difficult position. While the labor market is cooling, inflation appears stubborn and could drift higher, limiting monetary policymakers’ flexibility. As a result, the Federal Open Market Committee is likely to hold policy steady for the foreseeable future.

Looking forward, if gasoline prices stabilize in the coming weeks, pressure on household budgets could begin to ease, providing some support for restaurant traffic and broader consumer spending. For restaurants, these dynamics point to continued resilience and modest growth in the year ahead. That said, persistent uncertainties—particularly around consumer sentiment and cost pressures—suggest that the outlook will remain cautiously optimistic, especially given that meaningful relief on gasoline prices remains far from certain at this point.

This article presents the latest trends in key economic indicators as well as an outlook for the year ahead. Visit this page throughout the year for the Association’s latest projections for the U.S. economy.

Job growth has rebounded in the early months of 2026

Nonfarm payrolls increased by a solid 115,000 in April, well above the consensus estimate of 55,000 and building on the revised gain of 185,000 in March. While job growth has fluctuated month to month through much of the second half of 2025, employment has risen in three of the past four months, resulting in a net gain of 304,000 so far this year. This performance is encouraging given the pervasive economic uncertainties and underscores the underlying resilience of the U.S. economy.

Unemployment rate remains historically low

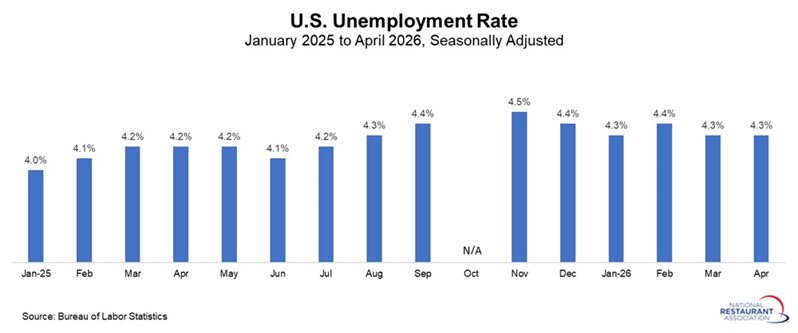

The unemployment rate remained at 4.3% for the second straight month, which has been the average since June 2025. Yet, the number of unemployed individuals was somewhat higher, up from 7.24 million in March to 7.37 million in April.

At the same time, the civilian labor force has contracted notably so far this year, declining from 171.50 million in December 2025 to just under 170.00 million in April. The labor force participation rate also edged down, slipping from 61.9% in March to 61.8% in April, the lowest level since October 2021.

This suggests that a meaningful share of potential workers has moved to the sidelines, posing an ongoing challenge for employers. Even as overall labor market conditions show signs of cooling, many businesses, including restaurants, will continue to struggle to find and retain talent.

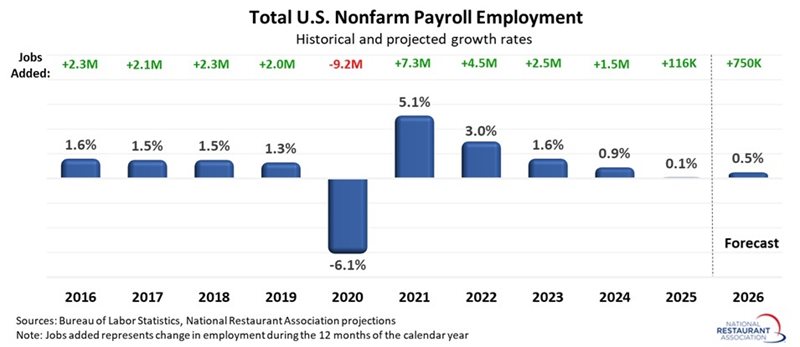

Economy projected to add 750,000 jobs in 2026

Job growth slowed materially in 2025, adding only 116,000 nonfarm payroll workers, the weakest annual job growth since 2020. Yet, there will be enough tailwinds in the economy, even with notable downside risks, for the labor market to generate a net 750,000 jobs in 2026. The national economy is projected to add a net 750,000 jobs during 2026. Despite more sluggish job growth in 2025 and 2026, it should represent the sixth consecutive year of nonfarm payroll employment growth, adding roughly 16.6 million jobs since the end of 2020.

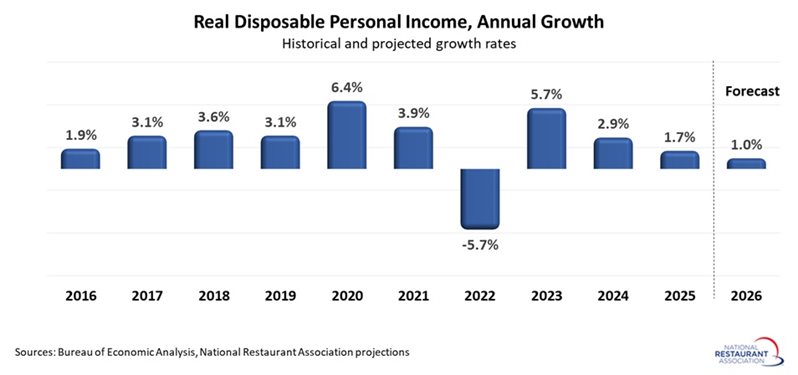

Personal income growth expected to slow

Wage growth is expected to continue in 2025, but decelerating employment gains will likely dampen the increase in aggregate income. Disposable personal income—a key driver of restaurant sales—is projected to increase at an inflation-adjusted rate of 1.0% in 2026. While still positive, that would be down from stronger growth of 2.9% in 2024 and 1.6% in 2025.

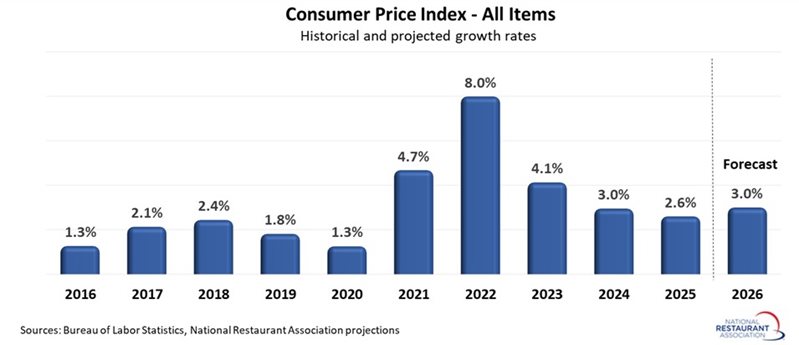

Inflation has trended higher this year

After peaking at 8.0% in 2022—the fastest annual increase in four decades—inflation has steadily moderated, though at a slower pace than many had hoped. While meaningful progress has been made toward the Federal Reserve’s 2% target, price pressures remain persistent in several categories. Entering 2026, inflation was expected to continue easing. Instead, higher energy costs tied to the war in Iran have pushed inflation modestly higher this year, interrupting that anticipated downward trend.

Should the conflict de-escalate and the Strait of Hormuz reopen, energy markets could stabilize, helping to stabilize broader price pressures. However, such relief may not materialize quickly. As a result, the National Restaurant Association now forecasts consumer price index growth of 3.0% in 2026, up from 2.6% in 2025.

Economic growth remains surprisingly resilient

Overall, the U.S. economy has remained surprisingly resilient despite numerous headwinds. Real Gross Domestic Product (GDP) should rise by 2.3% at the annual rate in 2026, up from 2.1% in 2025.

At the same time, consumer confidence has fallen sharply, reaching a record low amid persistently elevated gasoline prices driven by the war in Iran. Even prior to the conflict, there were clear signs of consumer strain, with many households struggling to make ends meet, placing greater emphasis on affordability and becoming more deliberate in their spending decisions. Restaurant operators are increasingly concerned that higher gasoline prices will weigh on traffic and sales while further squeezing already tight profit margins. These pressures could be exacerbated if inflation remains elevated.

To be sure, there are also positive factors helping to mitigate these risks. Equity and housing values remain at or near all-time highs, and wages continue to rise at healthy, albeit moderating, rates. The “K-shaped” nature of consumer spending remains evident, supporting overall resilience, particularly among higher-income households. Meanwhile, larger tax refunds have provided some temporary relief, helping to offset higher costs associated with gasoline and other essential goods.

The labor market itself has been somewhat choppy. While hiring slowed in the second half of 2025, nonfarm payrolls increased by a solid 115,000 in April, with gains recorded in three of the first four months of 2026. We forecast that the U.S. economy will add approximately 750,000 net new jobs this year—a slower pace than in recent years but still indicative of underlying economic durability. At the same time, the unemployment rate remains historically low.

Looking ahead, the National Restaurant Association forecasts real GDP growth of 2.3% in 2026, slightly above the 2.1% pace expected for 2025. This outlook reflects continued resilience despite geopolitical risks and heightened caution among consumers and businesses. Growth has been supported in part by strong investment in artificial intelligence and data infrastructure, even as spending in other areas—particularly goods—has slowed or stalled.

Inflation, however, remains a complicating factor. Prices are expected to trend somewhat higher in the near term, placing the Federal Reserve in a difficult position. While the labor market is cooling, inflation appears stubborn and could drift higher, limiting monetary policymakers’ flexibility. As a result, the Federal Open Market Committee is likely to hold policy steady for the foreseeable future.

Looking forward, if gasoline prices stabilize in the coming weeks, pressure on household budgets could begin to ease, providing some support for restaurant traffic and broader consumer spending. For restaurants, these dynamics point to continued resilience and modest growth in the year ahead. That said, persistent uncertainties—particularly around consumer sentiment and cost pressures—suggest that the outlook will remain cautiously optimistic, especially given that meaningful relief on gasoline prices remains far from certain at this point.

This article presents the latest trends in key economic indicators as well as an outlook for the year ahead. Visit this page throughout the year for the Association’s latest projections for the U.S. economy.

Job growth has rebounded in the early months of 2026

Nonfarm payrolls increased by a solid 115,000 in April, well above the consensus estimate of 55,000 and building on the revised gain of 185,000 in March. While job growth has fluctuated month to month through much of the second half of 2025, employment has risen in three of the past four months, resulting in a net gain of 304,000 so far this year. This performance is encouraging given the pervasive economic uncertainties and underscores the underlying resilience of the U.S. economy.

Unemployment rate remains historically low

The unemployment rate remained at 4.3% for the second straight month, which has been the average since June 2025. Yet, the number of unemployed individuals was somewhat higher, up from 7.24 million in March to 7.37 million in April.

At the same time, the civilian labor force has contracted notably so far this year, declining from 171.50 million in December 2025 to just under 170.00 million in April. The labor force participation rate also edged down, slipping from 61.9% in March to 61.8% in April, the lowest level since October 2021.

This suggests that a meaningful share of potential workers has moved to the sidelines, posing an ongoing challenge for employers. Even as overall labor market conditions show signs of cooling, many businesses, including restaurants, will continue to struggle to find and retain talent.

Economy projected to add 750,000 jobs in 2026

Job growth slowed materially in 2025, adding only 116,000 nonfarm payroll workers, the weakest annual job growth since 2020. Yet, there will be enough tailwinds in the economy, even with notable downside risks, for the labor market to generate a net 750,000 jobs in 2026. The national economy is projected to add a net 750,000 jobs during 2026. Despite more sluggish job growth in 2025 and 2026, it should represent the sixth consecutive year of nonfarm payroll employment growth, adding roughly 16.6 million jobs since the end of 2020.

Personal income growth expected to slow

Wage growth is expected to continue in 2025, but decelerating employment gains will likely dampen the increase in aggregate income. Disposable personal income—a key driver of restaurant sales—is projected to increase at an inflation-adjusted rate of 1.0% in 2026. While still positive, that would be down from stronger growth of 2.9% in 2024 and 1.6% in 2025.

Inflation has trended higher this year

After peaking at 8.0% in 2022—the fastest annual increase in four decades—inflation has steadily moderated, though at a slower pace than many had hoped. While meaningful progress has been made toward the Federal Reserve’s 2% target, price pressures remain persistent in several categories. Entering 2026, inflation was expected to continue easing. Instead, higher energy costs tied to the war in Iran have pushed inflation modestly higher this year, interrupting that anticipated downward trend.

Should the conflict de-escalate and the Strait of Hormuz reopen, energy markets could stabilize, helping to stabilize broader price pressures. However, such relief may not materialize quickly. As a result, the National Restaurant Association now forecasts consumer price index growth of 3.0% in 2026, up from 2.6% in 2025.

Economic growth remains surprisingly resilient

Overall, the U.S. economy has remained surprisingly resilient despite numerous headwinds. Real Gross Domestic Product (GDP) should rise by 2.3% at the annual rate in 2026, up from 2.1% in 2025.