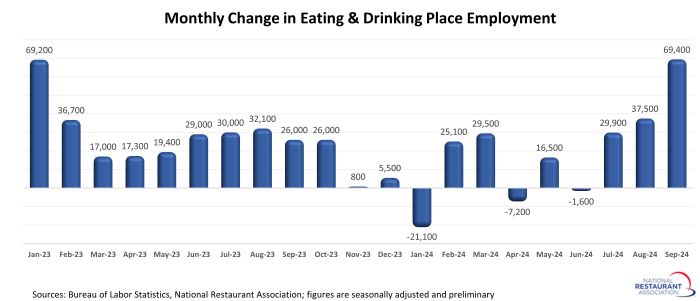

Restaurants added nearly 70k jobs in September

Job growth in the restaurant industry regained momentum in recent months, with September’s payroll expansion representing the largest monthly increase in more than two years.

Eating and drinking places* added a net 69,400 jobs in September on a seasonally-adjusted basis, according to preliminary data from the Bureau of Labor Statistics (BLS). That followed upward-revised gains of 29,900 jobs in July and 37,500 jobs in August.

In total for the third quarter, eating and drinking places added a net 136,800 jobs. That represented the largest quarterly employment growth since the third quarter of 2022 (+196,900 jobs).

The third quarter’s resurgence was also a solid improvement over the second quarter, when employers added fewer than 8,000 positions.

It’s important to note that preliminary employment reports have been volatile and subject to sizable revisions in recent months. However, the latest readings suggest that restaurant operators continue to have a healthy demand for employees, and that the second quarter’s softness was not the beginning of a broader downturn.

As a result of the solid gains in recent months, the gap between the industry’s current staffing counts and pre-pandemic levels continues to widen. As of September 2024, eating and drinking places were 179,000 jobs (or 1.5%) above their February 2020 employment peak.

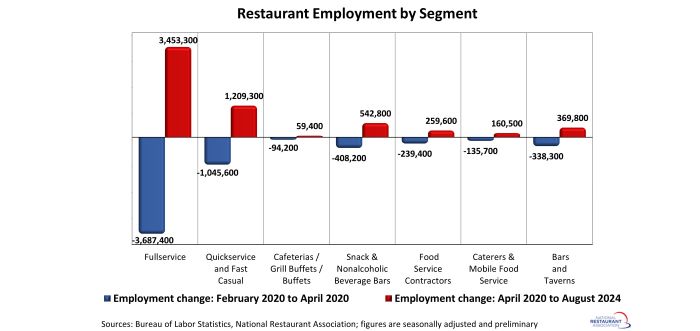

Fullservice segment still down 234k jobs

While the overall restaurant industry surpassed pre-pandemic employment levels, significant differences still exist by segment.

The fullservice segment experienced the most job losses during the initial months of the pandemic – and it still has the longest path to recovery. As of August 2024, fullservice restaurant employment levels were 234,000 jobs (or 4%) below pre-pandemic readings in February 2020.

Employment counts in the cafeterias/grill buffets/buffets segment (-32%) also remained below their February 2020 levels.

Job losses in the limited-service segments were somewhat less severe during the initial months of the pandemic, as these operations were more likely to retain staff to support their existing off-premises business. As of August 2024, employment at snack and nonalcoholic beverage bars – including coffee, donut and ice cream shops – was nearly 135,000 jobs (or 17%) above February 2020 readings.

Staffing levels in the quickservice and fast casual segments were nearly 164,000 jobs (or 4%) above pre-pandemic levels. Headcounts at bars and taverns were 32,000 jobs (or 7%) above the pre-pandemic peak.

[Note that the segment-level employment figures are lagged by one month, so August is the most current data available.]

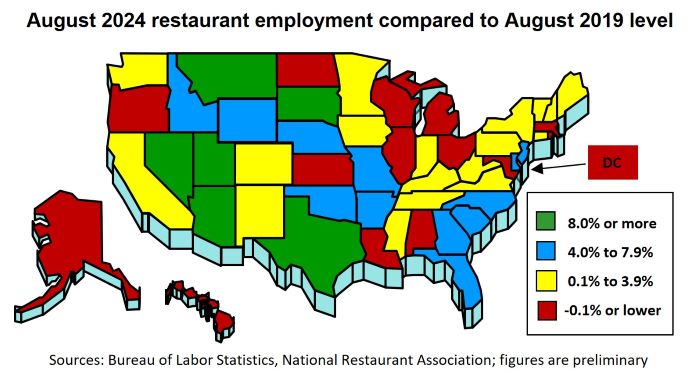

Restaurant job growth varies across the states

Restaurant employment trended higher in recent months, but the extent of the industry’s workforce recovery varies significantly by state. As of August 2024, 14 states and the District of Columbia had fewer eating and drinking place jobs than they did in August 2019.

This group was led by Maryland and Louisiana, which had 7% fewer eating and drinking place jobs in August 2024 than they did in August 2019. Oregon (-5%), North Dakota (-5%) and the District of Columbia (-5%) were also well below their pre-pandemic restaurant employment levels.

As of August 2024, eating and drinking place employment in 36 states surpassed their comparable pre-pandemic readings in August 2019. This group was led by South Dakota (+15%), Montana (+13%), Nevada (+13%) and Utah (+12%).

[Note that the state-level analysis uses August 2019 as the pre-pandemic comparison instead of February 2020, because seasonally-adjusted employment figures are not available.]

*Eating and drinking places are the primary component of the total restaurant and foodservice industry, providing jobs for roughly 80% of the total restaurant and foodservice workforce of 15.5 million.

Read more analysis and commentary from the Association's economists.